BTC ETF-mania: Bought the Mystery, Sell the History?

Expecting the BTC ETF approvals to be a major sell-the-news event.

With the November CPI print, the last major macro catalyst of the year has passed. There are ~25 days between now and the the ETF decision. Here’s how I see things playing out for BTC for the rest of the year.

Thesis: I expect BTC to drift higher into the ETF announcement, and then sell off violently.

MACRO FACTORS

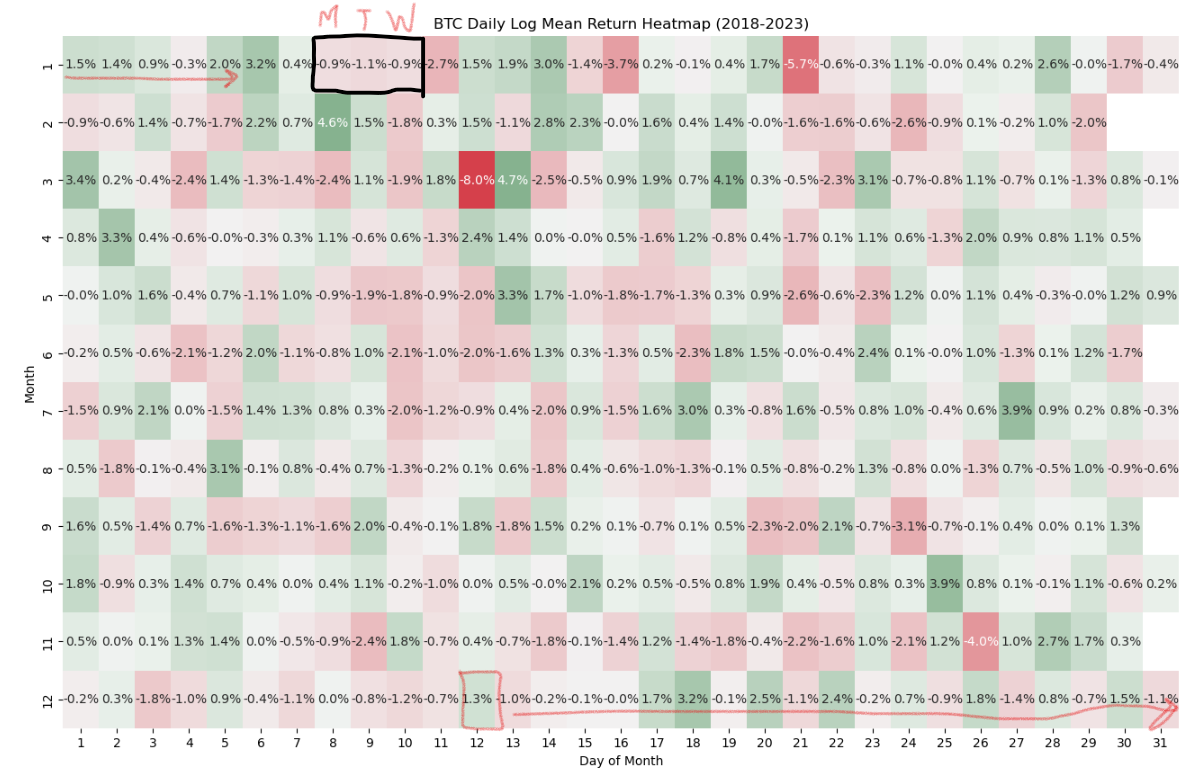

Seasonality

Based on seasonality alone, BTC’s expected return profile between now and January 8-10 (the weekdays in the Jan 5-10 window where approval can be announced) looks increasingly bullish with each passing day.

The first caveat to that comment is that BTC’s % performance YTD is basically tied with 2020, BTC’s best year by far as a “mature asset.”

The second caveat is that BTC’s 2020 performance was so strong that it warped seasonality for the asset. Ex 2020, BTC’s expected return in December is fairly weak.

The third caveat is that BTC’s returns this year are a lot more of an aberration than 2020. In 2020, US stimulus payments were far higher, interest rates were at zero, real interest rates were deeply negative, and BTC’s most relevant tradfi comparables (gold & Treasuries) returned a very strong +20% and +~15% respectively.

Overall, given low bond/equity volatility in December and the presence of a big expected positive catalyst in January, I don’t see any compelling reason to argue against BTC seasonality.

Conclusion: BTC’s short-term risk/reward is increasingly favorable, especially if it weakens more over the next couple of days.

Inflation & USD rates

The November CPI print was a relative non-event, although core inflation stopped improving y/y.

The big narrative underpinning the 2023 crypto bull market (besides the ETFs, court victories, and April 2024 halvening) has been a very strong conviction that interest rates must go down in 2024. I don’t understand where the conviction in this view comes from.

As I’ve argued on Twitter, I believe the Truflation CPI methodology has a laggy, but very significant lead over official US CPI. Truflation has >10 million daily price inputs, a much more dynamically updating consumer goods basket, much better ways of tracking apples-to-apples changes, and accounts for changes in rents properly, and has no possible institutional incentives for under-reporting inflation or making abrupt, dubious methodological changes, such as the BLS’s recent major change to how it accounts for US healthcare inflation (which took 20-30bps off of ongoing inflation readings). However, ex housing, Truflation and CPI are highly directionally correlated.

Truflation showed that US inflation clearly bottomed over the summer at 2%. Despite unprecedented dumping of the US strategic oil reserve, a deepening Chinese economic slowdown, and generally-soft oil prices, inflation has crept higher across most major categories in 4Q.

The combination of a slight upward creep in most of the CPI basket, stable asset prices, and drastically toughening year-over-year comps basically guarantee a rip higher in inflation in 2Q, which should be quite bearish for crypto prices (absent a recession, which would initially also be very bearish). US households have run down most to all of their pandemic excess savings, and more corporate CEOs are citing marginally softening consumer demand on earnings calls.

A US oil reserve rebuild, Chinese economic rebound, or seemingly-inevitable escalation between Israel and Iran would aggravate an already-lousy inflation outlook.

The obvious stopgap solution to these issues — cutting government deficit spending to relieve pressure on bond prices and boost USD values — is not bullish for crypto. Crypto is among other things a bet on government stupidity staying the same or getting worse; higher deficits are bullish for crypto and equities, and lower deficits are bearish crypto, despite being bullish for bonds.

All that said, while these issues are a big cloud hanging over crypto in the February-May timeframe, they’re a non-issue for the next 25 days.

Conclusion: Inflation & rates pose a huge headwind to crypto starting in March.

Momentum

A very simple BTC momentum strategy (go long a 168-hour closing high, go short a 168-hour closing low) would’ve returned almost 50% since 1/1/2022, near the peak of the last bull market. (red area = short BTC based on this rule, green area = long; funding cost assumed to be zero.)

Short-term momentum flipping bearish into seasonal softness in front of a major positive catalyst feels noisy to me (i.e., a low-to-medium conviction buying opportunity). On the short side, momentum signals have misfired all year long, even during periods when BTC was weak for weeks.

Conclusion: BTC momentum is taking a breather, but not in a way that signals some kind of tradable (to me) regime change.

Altcoins & new crypto products

Going long momentum doesn’t work nearly as well in alts as it does in BTC. There are many reasons for this, but altcoins share many governance drawbacks with SPACs and ADRs (this is a topic for another post). 95%+ of them grind to zero over time.

A strategy of going long the 20 strongest-momentum altcoins out of a list of 55-100 relatively liquid altcoins (the list grows with time as more alts get listed) (equal-weight, no txn costs, rebalance every 24 hours) over the past 2 years would still be in a deep drawdown.

The above—starting from 2 years ago, when BTC was $48,000 — assumes a starting capital of $10,000, so it would still be down around 35%, even after a 100% rally over the past 3 months.

Now: Is this justified? I think so. Put differently, the altcoin market doesn’t seem crazy-bullish yet relative to history.

Crypto Product Market Fit (PMF) so far this cycle has disappointed. I blame this entirely on US regulators cutting off smart contracts from USD interoperability. Smart contracts which can’t oversee anything offchain are limited to gamblefi applications (dexes). The longer I have been involved in crypto, the more convinced I am that the US legal system is the only one that can provide the global, offchain reach that can allow blockchains to achieve anything close to their full potential in terms of unlocking real-world value.

Other crypto products with great promise, like Real World Asset tokenization and securitization, require USD interoperability to deliver meaningful benefits (tokenization of non-standardized assets) relative to their currently artificially-extreme operational, iterative, legal, and working-capital costs.

Conclusion: Although SOL, Cosmos, Avalanche and other alt ecosystems have laid the technical groundwork to unlock new use-cases, no new Big Unlocks seem imminent outside of a second stab at web3 gaming, which gamers have already panned many times.

POSITIONING

Demand for a BTC ETF product

The biggest question by far, though, is: What problems do BTC ETFs solve that aren’t currently solved by other regulated investment vehicles?

GBTC, which any American can buy in their 401(k) account today, now faces extremely similar legal issues to ETF approval. It trades at a 9-12% discount to NAV, which I interpret as the market giving 90% odds of ETF approval in January and 2% odds of the SEC blindsiding everyone with a material delay or rejection.

GBTC has 2% annual fees, which seem criminal until you realize that every new ETF will have fees of at least 1.2% (the Coinbase custody fee charged to all ETF providers), plus their own fees on top. Those fees will probably be very low at first for competitive reasons, but as the different ETFs consolidate, that will probably be at least another 30bps of fees. The end state of 1-2 ETF products charging 1.5% isn’t materially different from where the market is today.

Another consideration is the $100B of BTC on Coinbase. This represents almost 15% of all BTC in existence. Some percentage of that is institutional, ETF-equivalent BTC, which wealthy older folks have bought & held without trading it at all. This is supported by Coinbase’s extremely low asset turnover compared to offshore exchanges.

As Meltem Demirors noted, gaining access to an ETF that can be offered via Schwab or Fidelity is still a Big Unlock for older people who are used to managing their wealth from 1-2 home screens and aren’t willing to switch between multiple different apps and interfaces to manage different assets. It’s also a Big Deal for RIAs to be able to officially market BTC as a product.

All of these things can stimulate ongoing demand for BTC. But none of them suggest a particularly big untapped demand for BTC now. Anybody who buys into the (extremely well publicized) Fiscal Dominance Thesis has been able to gain BTC exposure with very little trouble.

Conclusion: BTC ETFs aren’t a major unlock relative to existing investment alternatives and what has already been bought in anticipation of this event.

Google Trends, App Downloads, Funding Rates

Worldwide search volumes for “bitcoin” and correlated cryptocurrency search terms are at post-bear highs, but nowhere near their bull-market peaks (which interestingly peaked 6 months before the end of the last bull market).

Similarly, Coinbase app downloads are extremely weak.

This tells me a couple of different things.

Current normie interest in crypto is somewhat low compared to prior crypto bull markets, and nowhere near manic.

Global normie interest in cryptocurrency is surprisingly weak, unless Google Trends is about to drop a big spike of an update.

Crypto needs to break out into genuinely new product categories to reignite normie interest comparable with the last bull market. Number go up won’t cut it.

Altcoin funding rates, while a bit elevated, also aren’t in nutty-bullish territory.

Conclusion: None / neutral.

American positioning

Conclusion: Americans are crowding into this trade, hard.

CONCLUSION

Seasonality suggests strength from Dec 15th into the days before the BTC event, and weakness after the event. Minor post-ETF headwind

The Soft Landing / Rate Hikes Are Over consensus appears extremely one-sided relative to all available evidence. This will probably start showing up in January CPI (c. Jan 12th) and will rapidly amplify into March. Major post-ETF headwind

BTC’s outperformance vs. bonds/stocks is much more extreme this year than 2020. Minor post-ETF headwind

US institutional investors already have multiple vehicles with which to gain BTC exposure, some of which (Coinbase) are heavily used by institutions. Minor post-ETF headwind

The BTC ETFs don’t change the bottom line for customers in terms of management fees to drastically expand the addressable market. Negative factor

The April BTC halvening and ETH ETF approvals are material, but well-understood and not-imminent, positive catalysts.

Crypto events always have a “buy the mystery / sell the history” dynamic to them. The burden of proof is on bulls to show why this event won’t trade that way, and all the evidence suggests to me that if anything the sell-the-news effect will be especially pronounced this time.