The “Mint Nothing and Burn 178bn LUNC Immediately” Option

Twitter: @4lex_4sh4w_TR

Twitter: @4lex_4sh4w_TR

The all-important 17th “burn page” of our original draft proposal, which in retrospect I should have put on the title page (only 22% of readers apparently made it that far) —

— carried the key presumption that the swap is disabled during this time, because that’s the most conservative / prudent approach to re-enabling the swap.

Which would mean that the first 140M USTN minted (using the USD $85M worth of LUNC taken from the Oracle Rewards Distributor, and converted to BTC, as no-mint collateral) wouldn’t burn any LUNC.

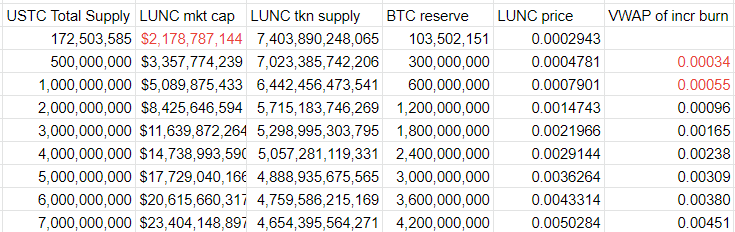

As the sheet in the original white paper showed:

However, if a) we repurposed LUNC from the Oracle Rewards Distributor solely to secure BTC collateral (thus not minting any new LUNC); and b) the LUNC-USTN swap were enabled from the start, then the burn wouldn’t start at 172.5M USTN of circulating supply — it’d start at 0, and 189bn LUNC would be burned during the process of minting the first 140M USTN (below). (141.5M * (1–60% CR) = $57M; $57M / .00032 = 178bn)

This carries its own risks. We’d be managing USTN live on-chain from the very beginning (although it wouldn’t be listed on other CEXs yet, so we’d have near-total control of on-chain liquidity, and our capital controls would be extremely robust). This will change over time as liquidity seeps to other venues, where we won’t control various aspects of capital controls, but in the beginning, we’d have near-total control over it.

But regardless, we’d need more on-chain use-cases for USTN to soak up USTN supply, like launching new on-chain liquidity pools, a new dex, etc. We’d need significant infrastructure that doesn’t currently exist. This will probably take more time to prepare, before the swap is re-enabled.

And most importantly (as in all our other proposals thus far), it would also require the total, or near-total, repeal of the current tax regime, which has destroyed on-chain liquidity, failed to live up to anything close to what it promised, and is living on borrowed time. We’re almost through 2 weeks of the promised 4 week Binance “charity burn,” and Binance basically said that they won’t continue the burn unless taxes are significantly cut or most/all other CEXs adopt Binance’s (extremely charitable) burn policy.

Anyway, while I think the community is focused on “burning” to a point that damages other long-term priorities (prudent risk management, ecosystem development, reeling USTC holders back into the ecosystem at a trivial customer acquisition cost, etc.), the ecosystem paralysis caused by the 1.2%-tax status quo is toxic enough for the chain that almost any other solution would be preferable, and a growing segment of the community seems to agree. If it requires notching up the risk level a gradient to give the community a burn that dwarfs whatever we’ll get from the CEXs — well, it can be done, and it’s probably worth the risk if it can partially or totally reverse the 90% loss in on-chain liquidity we’ve seen from the 1.2% tax.

Implications of Using the Oracle Rewards Distributor (ORD) Funds

Vegas argued the other day that using the Oracle Rewards Distributor as the source of BTC collateralization was dangerous, presumably because it would deplete oracle rewards for validators, reduce incentives to stake, and potentially jeopardize network security. This criticism is technically correct but IMO it misses the mark for several reasons.

The ORD is a static pool of capital that’s being drained at a nonlinear (front-loaded) rate. It needs a working dual-token swap system in order to be replenished. The status quo simply drains the ORD to the benefit of the 9% of LUNC staked to validators. (Vegas, as a validator himself, is a direct beneficiary of this unsustainable status quo.)

Stakers and validators, under this proposal, would thus be surrendering very rich short-term rewards to ensure the long-term health of the chain.

Anybody who cares about the long-term health of the ecosystem needs to either propose an annual inflationary rewards system to compensate stakers/validators (common in other proof-of-stake chains, including LUNA 2.0, but probably not politically possible, and totally unacceptable to Vegas’s political party), or agree to restore some form of the dual-token system using existing resources. Saying “I don’t like this solution” is simply arguing for an unsustainable status quo, and we’re running out of time to do something about it.

We could just issue a fraction of the initial 189bn of LUNC burn back into the ORD pool if we wanted, to make validators somewhat whole again (but significantly reduce the initial burn amount).

Anyway, the point is that the status quo is unsustainable. Alternative solution proposals are more than welcome. Criticisms along the lines of “I don’t like this idea and I don’t have any alternatives to the the current status quo” aren’t constructive or sustainable.

If you don’t want minting, there are ways to launch a revitalized dual-token mechanism without minting (if action is taken soon). If you can live with a little minting, all kinds of possibilities open up. But if we do nothing, the ecosystem will die (it’s on life support already) and the token will die.