Helicoptering Everclear to the Punch Bowl

A hawkish charade ends ignominiously, as fiscal dominance takes center stage

I wrote 2 days ago that with the CPI release, the last major catalyst for 2023 had passed, because Powell makes it a point to not surprise markets.

Except when he makes a point to surprise markets.

In hindsight, there are 2 schools of thought with regard to Jerome Powell.

Powell wants to be Paul Volcker incarnate. However, Powell has to work with a FOMC that’s extremely stacked with Democrats and doves. (By my count, out of 11 full members and 5 alternate members, the only hawkishly-inclined FOMC members today are Powell, Bowman, Waller, and Logan.)

Powell can only push hawkish policy when severe external pressure turns dovish Democrats into opportunistic hawks, i.e., the Democratic Party’s overriding political priority is reducing inflation, as in 2022 through 2Q23. During these periods, Fiscal Dominance is temporarily kicked out of the driver’s seat.Powell just follows the bond market.

After yesterday’s Big Bang to the bond market, (1) is the only Jerome Powell model that holds predictive power, imo.

Regardless, the Fed and its 1000 unaccountable, $500k/year economists have shown, just as they did in the summer of 2021, that they have no understanding of how year-over-year comps and lags flow into US CPI.

Truflation, which has much more real-time data than the US CPI methodology does, led US deflation lower throughout 2023 and bottomed out at 2% in June/July. The gap between US government CPI and Truflation data, however, has basically disappeared.

Housing (34% of US CPI), which Truflation measures concurrently and which the US government measures with a 6-12 month lag vs. reality, has seen no drop in inflation in 6 months, and will re-accelerate if rates stay near current levels.

Back in the day, I downloaded Zillow monthly rent across all US metros to compute market-weighted average rent increases year-over-year. I don’t do that anymore because ApartmentList does it for us. Their data is a bit higher-variance but extremely highly correlated with Zillow’s.

ApartmentList US rents YoY since 2018:

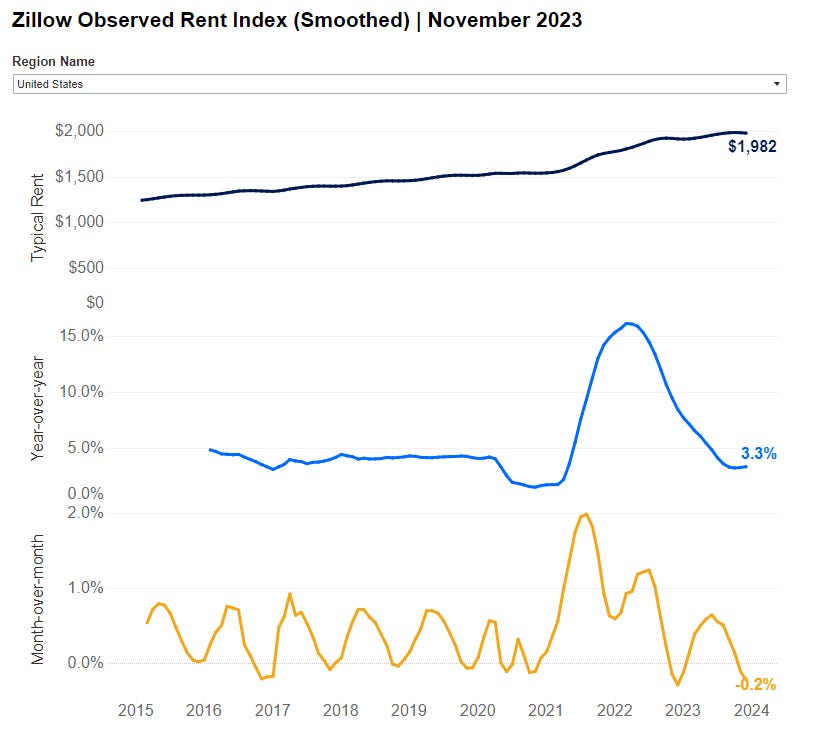

Zillow maintains a larger database which I used to scrape myself. One of these days I’ll update my scrapers to scrape and read it again. In the meantime, though, they summarize this data well. I believe Zillow’s dataset is the closest to the “lived experience” of the US national rental market. As you can see, its YoY trend is highly correlated to AL’s, but smoother:

The BLS, otoh, calculates CPI rent as basically a trailing 12 month average of 4 quarterly surveys of a random sample of the same 80,000 or so households. The BLS’s clearly-inferior methodology pegs rent inflation at 6.7% today.

Health insurance (.53% of the US CPI basket—lol, for my family of 3, monthly healthcare premia not covered by the employer are something like 3% of HH income not including copays, but I digress—deflating at 20-30% y/y according to the US government) saw an unexplained methodology change 2 months ago which created 15-20bps of annual deflation out of thin air.

All of this deflation came with an energy-commodity dividend amidst the Biden Administration’s squandering of the SPR, and extremely poor Chinese economic performance which is bound to mean-revert at some point in 2024.

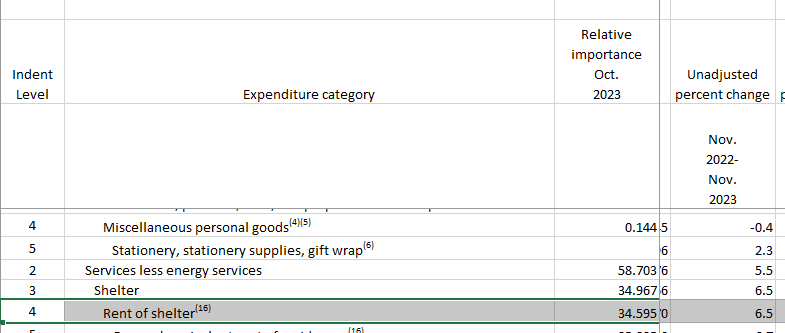

The BLS survey, despite a methodology rigged to exaggerate deflation in healthcare and housing over the next quarter or so, is picking up on many of the same inflationary pressures that Truflation and other sources are. Core inflation was flat MoM at 3.2%, well above the Fed’s 2% target.

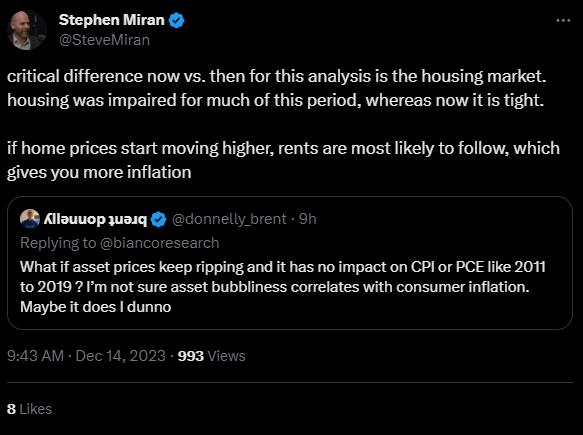

https://twitter.com/SteveMiran/status/1735309468563361947

Against these statistical realities, the Fed’s decision to join the global inflationary victory lap has no intellectually honest explanation.

Meanwhile, there is no planet on which US financial conditions are “restrictive.”

The S&P 500 forward P/E of 19, excluding the 2020-21 valuation bubble, is near 20-year highs. The smaller-cap indices have much more depressed P/E’s, although that’s mostly explained by their debt servicing costs and the skyrocketing cost of debt over the past year.

Except … that the cost of US government debt is actually virtually unchanged over the past year (2-year and 10-year rates are now basically unchanged since EOY 2022).

“But what about real rates?,” I can hear you asking. I know more bond traders who don’t take TIPS seriously than those who do.

Financial inflation, IRL inflation, and next-6-months inflation

Because US government policy is mostly a corrupt Cantillon effect of sloshing government spending to incompetent-but-superconnected private-equity operators like Dianne Feinstein’s late husband, US “stimulus” invariably results in substandard products delivered at exorbitant prices. These individuals then funnel their profits into paper financial assets (bonds, stocks, and vacation homes). Furthermore, these financial assets are mostly owned by a relatively small number of older people whose individual consumption is capped.

Thus, US government policy mostly stimulates status consumption for older, wealthier Americans, eg, Hermes purses and trophy properties in the Hamptons, Georgetown and Martha’s Vineyard. (And liberal economists remain doggedly confused about why workers think government spending is stupid, and why paper “GDP per capita” doesn’t translate into higher approval ratings for their anointed ones.)

The big exception was COVID, when the Fauci Trump Administration paid businesses to rack up bad debts on Uncle Sam’s dime and paid everyone else to sit on their couch for 6 months. This created a domestic demand explosion alongside a global supply crunch, and was the first time in living memory that “stimulus” trickled down to the real world.

Biden Administration policy has reverted to Obama-era crony capitalism: indiscriminate subsidies for wasteful healthcare consumption, renewable energy that never delivers, “rural broadband” grossly inferior to & more expensive than Starlink, etc.

All of this is a long-winded way of saying that yesterday’s Powell Pivot will pour gasoline on the fire of over-levered, under-earning financial assets.

Normally, that’s not a problem. It’s a stimulus for rich people that’s invisible to anybody who doesn’t have to plan for a family’s future (spending on a house, college, etc, as opposed to restaurants and IG moments) or pay for kids.

But as I argued yesterday, the groundwork has already been laid for a rebound in ‘official’ inflation in 2Q and especially 3Q. The Powell Pivot makes it a near-certainty that the key driver of rent deflation (private-equity firms going bankrupt and self-liquidating) is done.

Key takeaway: Clear skies ahead to long crypto into ETF. 1Q melt-up of garbage, leveraged assets into a violent 2Q/3Q hawkish pivot by a behind-the-curve Fed.